Why Atlanta Condo Master Policy Premiums Are Exploding in 2026 —

What Your Board Can Actually Do About It

By Brent Dixon, Licensed P&C Commercial Insurance Advisor · The Dixon Agency LLC / B. Dixon Risk Management · bdixonrisk.com

Atlanta condo boards are facing 30–90% master policy increases, new wind/hail deductibles, and non-renewals in 2026. Here’s why it’s happening, what Georgia law requires, and a board-level action plan to get your renewal under control.

If you sit on a condo board or manage associations in Atlanta, you’ve probably had a version of this phone call in the last twelve months:

Board president: “Our master policy renewal just came in. It’s up 38 percent. We already raised dues last year. The owners are going to lose their minds.”

Insurance advisor: “You’re not alone — and more importantly, you’re not stuck. But we need to start working this now, not thirty days before the renewal date.”

That conversation is happening all over the metro right now. One Buckhead condominium specialist reported his own building’s fees jumping 46 percent for 2026, pushing monthly costs above a dollar per square foot — and he called that “pretty typical” for buildings of that era. Atlanta HOA fees overall have climbed at double-digit rates, among the fastest in the country. And the single biggest line item driving those increases, in building after building, is the master insurance policy.

This article explains exactly why this is happening to Atlanta associations in 2026, what Georgia law actually requires your board to carry, and — most importantly — the specific steps a board can take in the next 90 days to change its outcome at renewal.

The short answer

Atlanta master policy premiums are surging because four forces hit at the same time:

- Georgia is one of the least profitable states in America for property insurers — ranked 50th out of 51 (states plus D.C.) for insurance company profitability. Carriers respond by raising rates, tightening underwriting, or leaving.

- Atlanta’s condo stock is aging into trouble. A huge share of intown buildings went up during the 2000–2003 development boom. Those buildings are now 20–25 years old — the exact age when roofs, elevators, plumbing stacks, and HVAC systems come due. Carriers know this.

- Storm losses keep stacking up. Hurricanes Idalia, Helene, and Milton, plus Georgia’s routine diet of hail, straight-line wind, and severe convective storms, have pushed reinsurance costs up — and those costs flow straight into your renewal.

- Underwriting got granular. Carriers now want reserve studies, roof documentation, updated valuations, and proof of maintenance before they’ll quote. Associations that can’t produce them pay more — or get non-renewed.

None of that is your board’s fault. But how your association responds to it is entirely within your control, and it’s the difference between a 10 percent increase and a 60 percent one.

What’s actually happening in the Atlanta market

Georgia’s carrier math is broken

Georgia is the tenth-largest state for property and casualty premiums, yet it sits at the bottom of the country for insurer profitability. When carriers consistently pay out more in claims than they collect in premiums, three things follow: rate increases, reduced capacity (carriers writing less business here), and outright market exits. Georgia’s Insurance Commissioner has publicly said he expects more companies to withdraw from the market.

For a condo association, “reduced capacity” isn’t an abstraction. It means the carrier that wrote your building for eight years suddenly won’t renew buildings over four stories, or over 20 years old, or with a roof past year 15 — and your broker has fewer places to take you.

The 2000–2003 building boom is coming due

Walk through Midtown, Buckhead, or Atlantic Station and you’re looking at a generation of buildings that all turned 20-something at the same time. Elevators, roofs, cooling towers, and original plumbing are hitting end-of-life together. That’s why fee increases of 40+ percent are showing up in that cohort specifically — deferred maintenance and insurance pressure compounding each other.

Here’s the part boards miss: carriers read your building’s age and maintenance history before they read anything else. A 2002 building with a documented roof replacement, updated systems, and a current reserve study is a completely different submission than the identical building next door with none of that paperwork — even if the buildings are physically similar.

Underwriting requirements that didn’t exist five years ago

Georgia condo associations now routinely see carriers:

- Requiring pre-inspections or engineer’s reports before releasing a quote

- Adding separate wind/hail deductibles (often 1–5% of building value) to policies that never had them

- Demanding updated statements of values and pushing back on limits that haven’t moved in years while construction costs have

- Asking for reserve studies and maintenance documentation as a condition of quoting

- Reducing or excluding coverages (earthquake, water damage sublimits) that used to be standard

A percentage wind/hail deductible deserves special attention. On a $20 million building, a 2 percent wind/hail deductible is a $400,000 out-of-pocket exposure per storm event. Many boards discover this only when a hailstorm hits — or when a unit owner’s lender flags it.

What Georgia law requires your association to carry

This is where a lot of board conversations go sideways, so let’s be precise.

For condominiums, the Georgia Condominium Act (O.C.G.A. §44-3-107) requires the association to carry:

- Property insurance on the buildings at full replacement cost

- Liability coverage of at least $1 million per occurrence / $2 million aggregate

- Annual budgets that include reserve line items for deferred maintenance and depreciation

What the statute does not regulate: deductibles, exclusions, wind/hail deductible structures, or premium increases. It also doesn’t require a formal reserve study or a specific funding level. And for non-condo HOAs under the Property Owners’ Association Act, there are essentially no statutory insurance requirements at all — your declaration is the controlling document.

Translation: the law sets a floor, your governing documents set the real requirements, and the market sets the price. Also note two changes on the horizon:

- SB 406 takes effect January 1, 2027, standardizing records access for Georgia associations — meaning owners will find it easier to demand and scrutinize your insurance documents, budgets, and minutes.

- Georgia’s Act 277 (2025) extended homeowners non-renewal notice from 30 to 60 days on the personal lines side — a signal of where regulators’ attention is. Commercial timelines differ, but the lesson is the same: non-renewal timing is tight, and boards that wait are the ones that end up in the surplus lines market at panic pricing.

Master policy vs. HO-6: the gap that turns into special assessments

Every premium conversation eventually becomes a coverage-structure conversation, because the cheapest way to “reduce” premium — quietly narrowing what the master policy covers — just moves cost onto your owners.

| Master Policy (Association) | HO-6 (Unit Owner) | |

|---|---|---|

| Building structure & common elements | ✔ Covered | — |

| Unit interiors (walls-in finishes) | Depends on policy form: all-in vs. walls-out/bare-walls | ✔ Should cover if master is walls-out |

| Personal property | — | ✔ |

| Master policy deductible passed to owners | — | ✔ via loss assessment coverage (if purchased, and only up to its limit) |

| Liability (common areas) | ✔ ($1M/$2M statutory minimum for condos) | Unit-level liability ✔ |

Two real-world failure modes I see constantly in Georgia associations:

- The walls-out surprise. The board switches to a bare-walls form to save premium. A pipe bursts, and owners discover their hardwood floors, cabinets, and drywall are their problem — and their HO-6 policies were sized for a walls-in world. Walls-out structures see dramatically more post-claim assessment disputes.

- The deductible pass-through. The association takes a $100,000+ deductible (or a percentage wind/hail deductible) to control premium, then a covered loss hits and the deductible gets specially assessed across owners — most of whom carry $1,000–$2,000 of loss assessment coverage, or none.

Neither structure is wrong. What’s wrong is doing it silently. If your board changes the master policy form or deductible, owners need written notice telling them exactly what to change on their HO-6 — before the loss, not after.

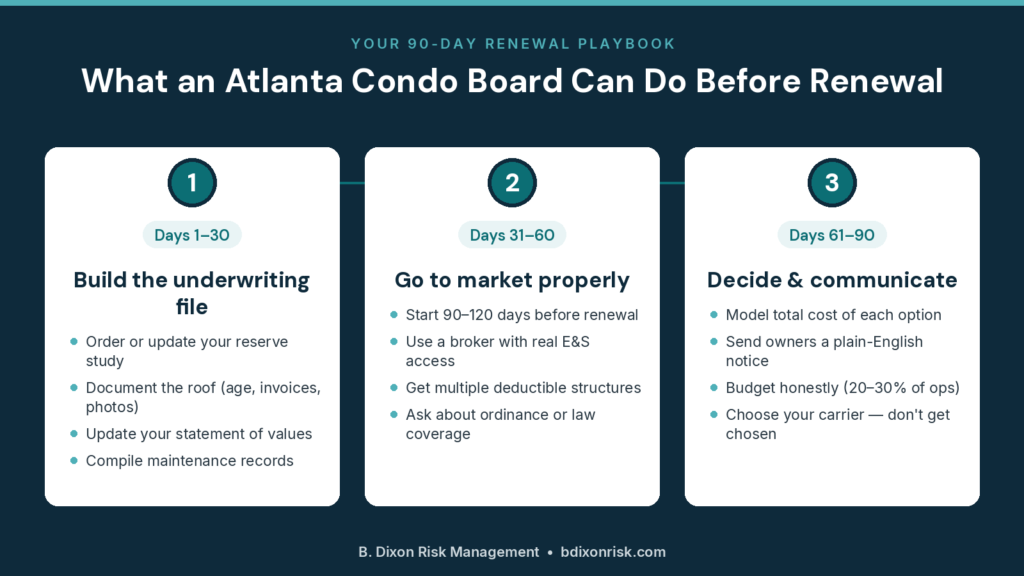

The 90-day renewal playbook for Atlanta boards

Here’s the process we run for associations, and what any board can start doing today.

Days 1–30: Build the underwriting file

- Order or update your reserve study. Even though Georgia doesn’t mandate one, carriers increasingly price as if it does. A current study plus a funded reserve line is the single strongest credibility signal you can send.

- Document the roof. Age, last replacement/repair, contractor invoices, photos. Roof age is the #1 property underwriting question in Georgia right now.

- Update your statement of values. If your building limit hasn’t moved in five years while construction costs jumped, you’re either underinsured or about to get flagged. Carriers penalize stale valuations with higher rates, coverage limitations, or refusal to quote.

- Compile maintenance records. Elevator inspections, plumbing work, fire system tests, water-mitigation devices (leak sensors genuinely matter to underwriters now).

Days 31–60: Go to market properly

- Start 90–120 days before renewal, minimum. The associations that get hurt are the ones shopping with three weeks left.

- Work with a broker who has real E&S (surplus lines) access. Much of Atlanta’s condo stock — older buildings, prior claims, aluminum wiring, tall frame construction — now prices better in the excess and surplus market than with admitted carriers. If your broker can only show you two admitted quotes, you’re not seeing the market.

- Get quotes structured multiple ways: different deductible levels, with and without percentage wind/hail, layered/shared limits for larger buildings. The premium spread between structures is often 20–40 percent.

- Ask about ordinance or law coverage. If your pre-2000 building suffers a major loss, current code will govern the rebuild. Parts A, B, and C of ordinance or law coverage fill the gap between “rebuild what was there” and “rebuild what the code now requires.”

Days 61–90: Decide and communicate

- Model the total cost of each option — premium plus realistic deductible exposure plus what it shifts onto owners’ HO-6 policies.

- Send owners a plain-English insurance notice: what the master covers, the deductible, what their HO-6 must now cover, and a recommended loss assessment limit. This one letter prevents most post-claim disputes — and most angry annual meetings.

- Budget honestly. Georgia associations now commonly spend 20–30 percent of their operating budget on insurance. Small buildings (6–12 units) often run $7,000–$15,000 a year; mid-size buildings $20,000–$50,000; large or high-rise properties $50,000–$225,000+. If your budget assumes last year’s number plus 5 percent, you’re planning to be surprised.

Five mistakes that make Atlanta renewals worse

- Shopping the policy every year with a different broker. Carriers see the submission churn and price defensively. Pick a broker with E&S depth and let them manage the market relationship.

- Filing small claims. A $9,000 water claim against a $25,000 deductible history can cost you multiples of that in premium and eligibility over the next five years. Use reserves for maintenance-sized losses.

- Letting the roof “age into trouble” undocumented. An 18-year-old roof with inspection reports and repair invoices is insurable. The same roof with no paperwork is a non-renewal.

- Ignoring the deductible when comparing quotes. The cheapest premium with a 5 percent wind/hail deductible can be the most expensive policy your association ever buys.

- Waiting for the non-renewal notice. By the time it arrives, your options are whatever’s left. Boards that market their program early choose their carrier; boards that wait get chosen.

Frequently asked questions

Our premium went up 40 percent with zero claims. How is that legal? Georgia law doesn’t regulate association premium increases. Your rate reflects the whole market — statewide carrier losses, reinsurance costs, storm trends, and your building’s risk profile (age, roof, valuation, reserves) — not just your claims history.

Can the carrier really demand an engineer’s report before quoting? Yes. Pre-inspections and engineering reports have become common conditions for quoting Georgia condo buildings, especially older or taller ones. Treat it as an opportunity: a clean report is leverage with every other carrier too.

What’s a reasonable wind/hail deductible for an Atlanta building? There’s no universal answer — it’s a trade between premium savings and assessment risk. What matters is that the board models the dollar exposure (percentage × building value), confirms owners’ loss assessment limits, and makes the choice deliberately.

Is the association required to insure unit interiors? For condos, it depends on your declaration and the policy form (all-in vs. walls-out). The Condominium Act requires full replacement cost on the buildings, but the walls-in/walls-out boundary is set by your documents and policy — which is exactly why owners need to be told which world they live in.

We got a non-renewal notice. How long do we have? Check the notice and your policy — commercial timelines vary, and they are short. Start marketing the account immediately, and expect the replacement placement to likely involve surplus lines carriers. (We’ll cover the full non-renewal playbook in a companion article.)

Will premiums come back down? The broader commercial market is stabilizing in 2026, and some Georgia carriers have even filed decreases in personal lines. But for condo property specifically, underwriting discipline — valuations, roof scrutiny, reserve documentation — is here to stay. Buildings that can prove they’re well-run will capture the softening first.

Your board’s next step

If your association’s renewal is inside the next six months — or you’ve already received an increase or non-renewal notice — the worst move is waiting to see what happens.

The Dixon Agency specializes in hard-to-place and surplus lines property programs for Georgia condo and homeowners associations. We’ll review your current master policy, your deductible structure, and your underwriting file, and tell you honestly whether your board is positioned well or exposed.

→ Request a free Master Policy Review → [Download: Atlanta Condo Board Insurance Renewal Checklist (PDF)] → Or call Brent Dixon directly: (786) 804-2580

Brent Dixon is a licensed property & casualty commercial insurance advisor serving the Atlanta Metro area, specializing in condo/HOA associations, contractors, restaurants, and hard-to-place commercial risks.